If you’re a vacation rental property owner or considering the purchase of one, you’ve likely asked yourself, “should I make my vacation rental an LLC?” The short answer is that there’s no right answer. There are many compelling factors that play a role in deciding whether or not to make your vacation rental a Limited Liability Company (LLC).

Every rental property owner has a unique financial situation that may require different advice. Here are a few reasons why you should or should not make your vacation rental an LLC.

An LLC’s Purpose is to Protect Your Assets

The main reason you may want to make your vacation rental an LLC is to protect your assets. An LLC protects you from a lawsuit, in the case your business faces circumstances such as bankruptcy. The risk of a hypothetical lawsuit is a serious consideration.

For example, despite your efforts to protect your renters’ safety, imagine if one of your renters was injured while staying at your rental. In this circumstance, you’re the one they may come after and, if they decide to pursue legal action, they will name you in their lawsuit. In this scenario, you would have to defend your personal assets.

If your vacation rental was under an LLC, only the LLC’s assets would be under attack.

LLCs Keep You Anonymous

If you prefer privacy, making your vacation rental an LLC may be a beneficial way to maintain your discretion. When you own a vacation rental, your name is on the deed, therefore potentially making it public knowledge who owns the rental.

If you would prefer to remain anonymous, an LLC may protect your privacy. If you live in a state that allows companies total anonymity, such as Wyoming or Nevada, it can be even more challenging to figure out who owns your vacation rental.

LLCs Come with Tax Advantages and Complexities

Opening an LLC can add to the complexities of filing your taxes. Working with a property management company, like TurnKey, can help ease the stress of tax time.

LLCs can be designated as various tax entities. If you’re considering an LLC, you would have your LLC taxed as a “pass-through” entity. Any income made from the vacation rental passes to the LLC’s owner or owners. This means that if you’re the sole owner of the vacation rental, you’ll more than likely pay taxes the same way you do now.

If you decide to set your LLC up as a “S” corporation or a “C” corporation, you may be able to reduce your taxes if you pay the self-employment tax. In this case you will wear two hats, the owner of the company and the employee. You will pay yourself as if you are an employee of your own company as well as reap the benefits of ownership.

Setting your LLC up in this manner may require a little bit more guidance from a tax professional. Consulting with a tax adviser prior to opening your LLC will help you determine if you should make your vacation rental an LLC.

Creating an LLC Costs Money

When forming a LLC there are costs involved. If you choose to use an incorporation website such as ZenBusiness, LegalZoom or IncFile, you could pay between $49 and $900. After paying the filing fees you will need to pay extra fees to obtain an employer identification number (EIN) and the operation agreement. The IRS requires all LLCs form within the state they reside in, not at a federal level. This means that laws and regulations may vary depending on the state. Certain states may have stricter requirements that may make it more challenging to set up an LLC.

In some states such as California, there is a required franchise tax. In California the franchise tax is $800 annually. There is also an additional fee for LLCs that are taxed as an “S” corporation or “C” corporation and have an operating income of equal or greater than $250,000.

Additionally, there may be some extra costs when it’s time to prepare your taxes. According to a recent survey conducted by the National Society of Accountants (NSA), the national average fee for tax preparation for an itemized 1040, Scheduled C Business Income, and a state return was $457.

If your rental property resides in another state other than the state you live in, you will need to determine which state you should file your LLC. If you only have one rental property in another state, you could consider forming your LLC in that state. But, if you decide to form an LLC in your home state but have a property in another state, you may need to qualify for intrastate business. This means that you may have to pay taxes and meet the laws of the other state. Each situation is unique and may require difference guidance.

When deciding if you should make your vacation rental an LLC, you will need to consider all costs involved. You may have some extra tax advantages with an LLC, but it will cost more to file correctly. You will need to determine if the extra cost is worth the reward.

Trouble Getting Property Financing

Acquiring proper lending may be another factor you should consider when asking yourself, “should I make my vacation rental an LLC?” When trying to purchase a single family home or duplex under the name of an LLC, some lenders may not approve the loan unless it’s under your name. They want their borrowers to be liable for the repayment of the loan in the case it were to default.

Some lenders may require you to purchase the entire property in cash if you wish the deed to be in the LLC’s name. However, you can try to change the name on the deed after you purchase the property.

It’s also possible that if you convert the ownership of your vacation rental to an LLC, your lender may require full repayment of the mortgage. This is commonly known as a due-on-sale-clause. This may not be a likely occurrence, but it’s something to consider when weighing out all of your options. There’s no guarantee that the lender won’t demand full repayment of the loan, which could require paying cash, refinancing, or selling the property.

Before making any decision, speak with your lender about their requirements. Understanding their requirements will help you make an educated decision if you decide to open an LLC.

Insurance Can Also Protect Your Assets

Rental property owners must purchase a dwelling policy. Since you’re required to purchase rental insurance anyway, you want to ensure it covers the proper limits. Depending on the insurance policy you purchase, your policy will pay cash value or replacement costs in the circumstance of catastrophic events.

It may also be wise to purchase an umbrella policy. Adding umbrella insurance to your dwelling policy can help protect your personal assets in the event you face legal action. Be aware that your insurance may not cover all costs. If this happens, your personal assets may be in jeopardy.

It’s important to understand what your policy will cover and what it won’t. Reviewing your policy details can help you determine what exclusions exist. You may not be willing to take that risk.

So, Should I Make My Vacation Rental an LLC?

You may still asking, “should I make my vacation rental an LLC?” As you can see, forming an LLC is a complex matter. You must weigh your risk tolerance against what you feel comfortable with when managing your property. If you want to limit your risk exposure, creating structure through an LLC entity may be the protection you seek. On the other hand, you may be content with the protection insurance you have and prefer to not maintain an LLC.

Each vacation rental owner has a different financial situation that may require different guidance and recommendations. It’s best to ask for guidance from your financial planner, CPA, or attorney to discover if an LLC is right for you.

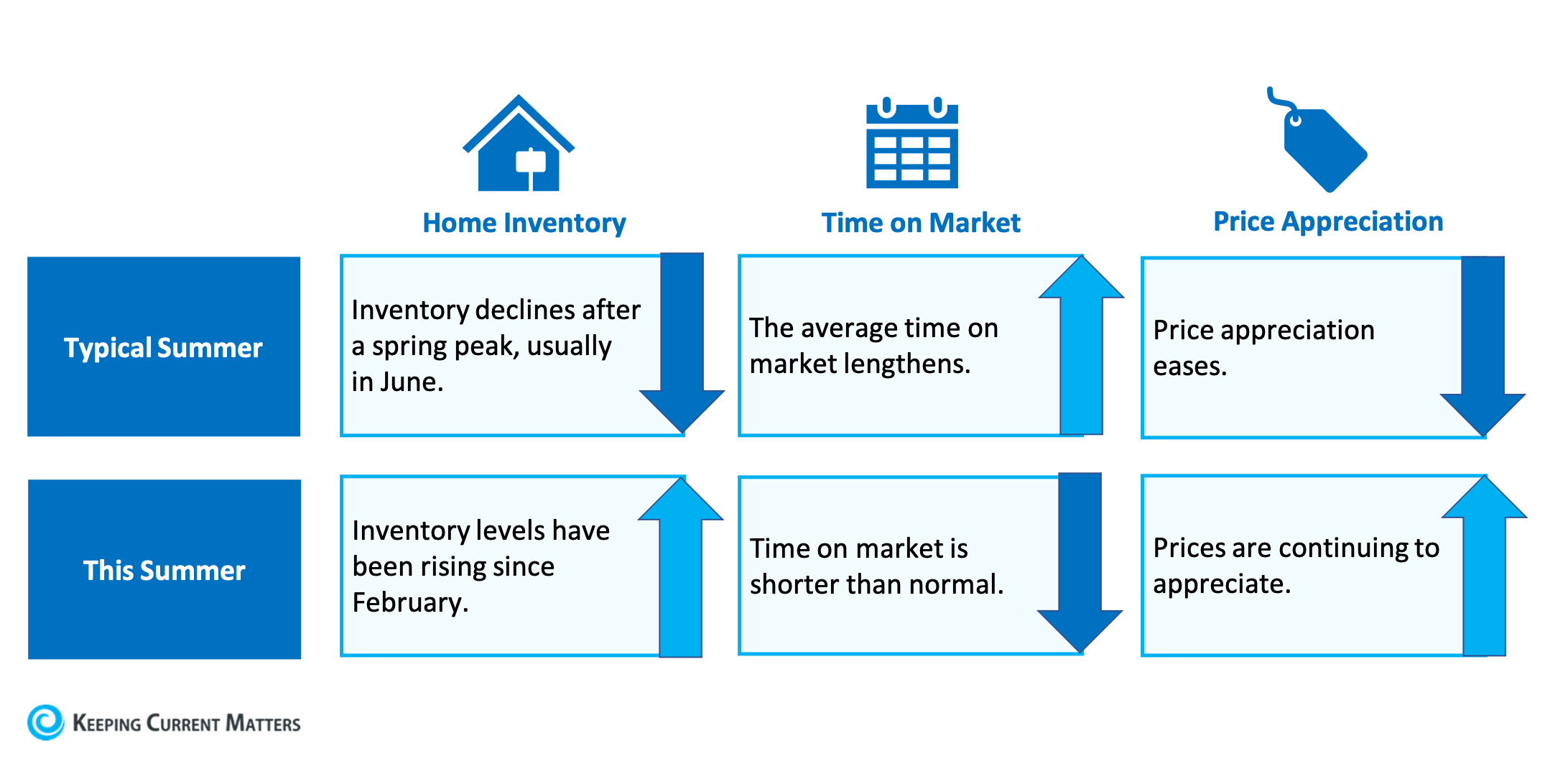

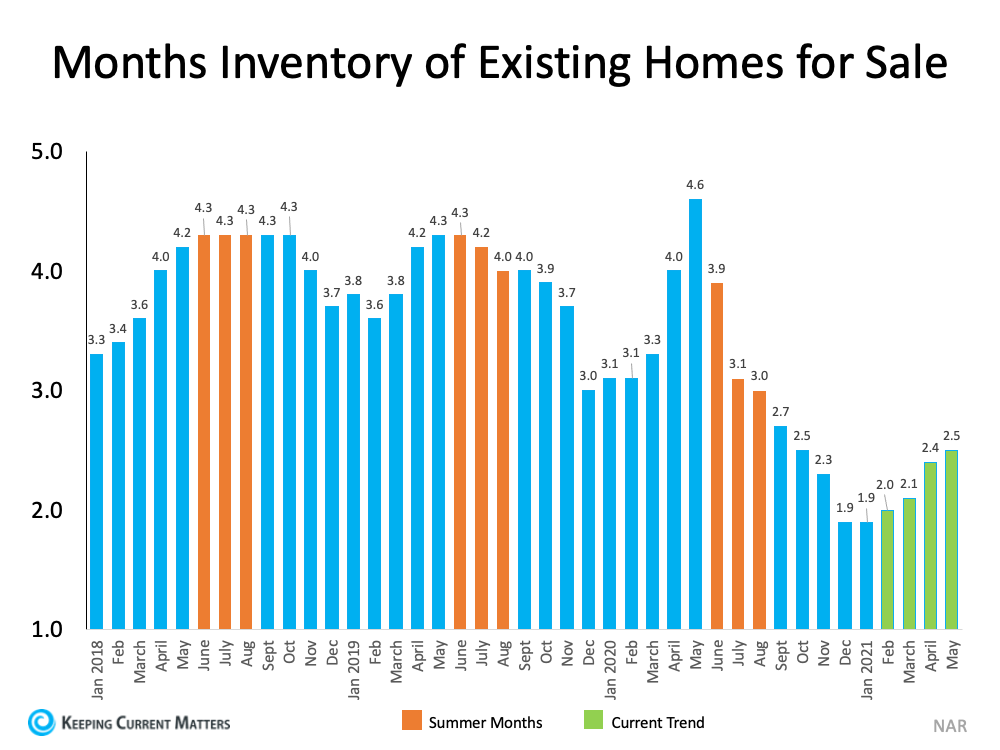

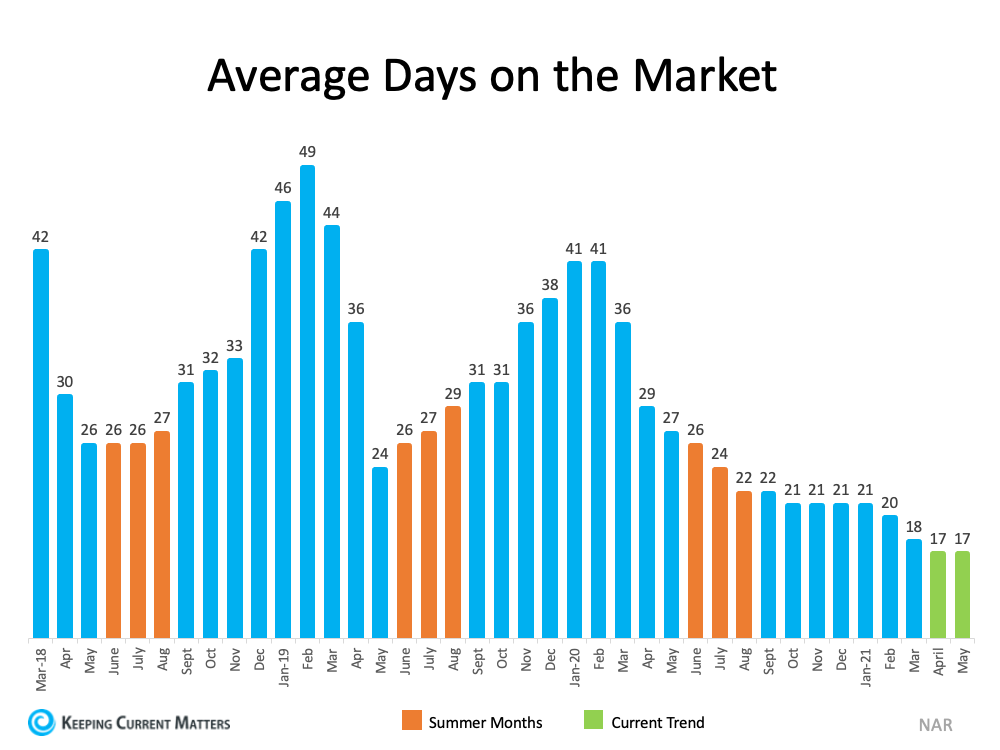

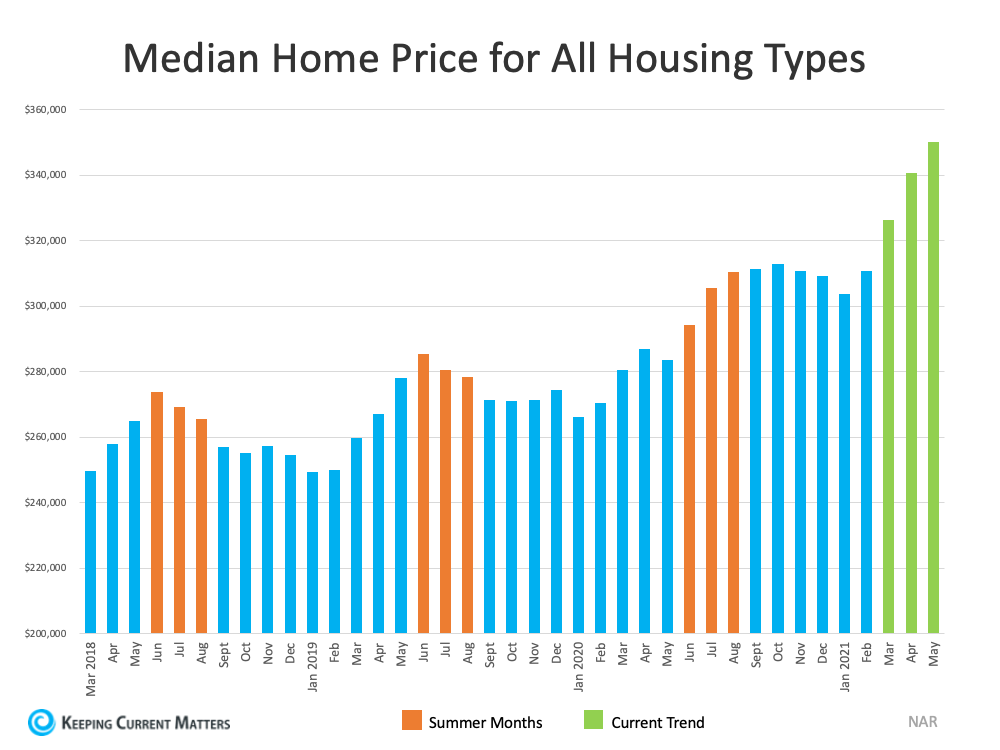

If you’re looking to buy, competition and bidding wars are driving prices up. Getting

If you’re looking to buy, competition and bidding wars are driving prices up. Getting